Welcome to Jayd Advisors!

Keep More Of What You Make,

& Really Live Your Life

With Tax Smart Financial Strategies

Smart Tax. Clean Books. Confident Growth.

Who is Jayd Advisors?

We Are Tax Planning Experts

Transforming Accounting & Tax Strategy into Growth Capital

Jayd Advisors empowers business owners and investors with a focus on maximized profit and minimized tax drag. Our goal? Turn tax strategy and financial management into fuel for business growth and personal wealth.

We Help You Craft a Holistic Plan

Your financial life is interconnected.

We design a comprehensive strategy that aligns your business, taxes, and personal wealth—ensuring all areas work together to support your goals, not against them.

We Identify Areas of Opportunity

We uncover overlooked opportunities for optimization and protection—whether it’s business structure, income planning, or asset protection.

Through our relationship with the Financial Gravity Family Office, we bring you exclusive tools and resources designed to elevate your financial strategy.

Ongoing Guidance and Support

Our partnership doesn’t end with a plan.

We stay by your side, offering consistent guidance, expert services, and responsive support as your life and business evolve—so you’re always prepared for what’s next.

Take The First Step

We provide personalized financial solutions and strategic guidance to help you reach your goals with clarity and confidence.

Start by taking our quick Needs Assessment by clicking the link below.

Once completed, our team will review your responses and invite you to a call to share tailored recommendations for your business.

Our Leadership Team

An Expert Team You Can Trust

Trust us to manage your finances and help you begin crafting your financial future with confidence.

Shelley R. Johnson, CPA

Lead Advisor & Tax Strategist

Deanna Johnson

Client Communications

Jorlena Dermody, CPA

Tax Strategist & Advisor

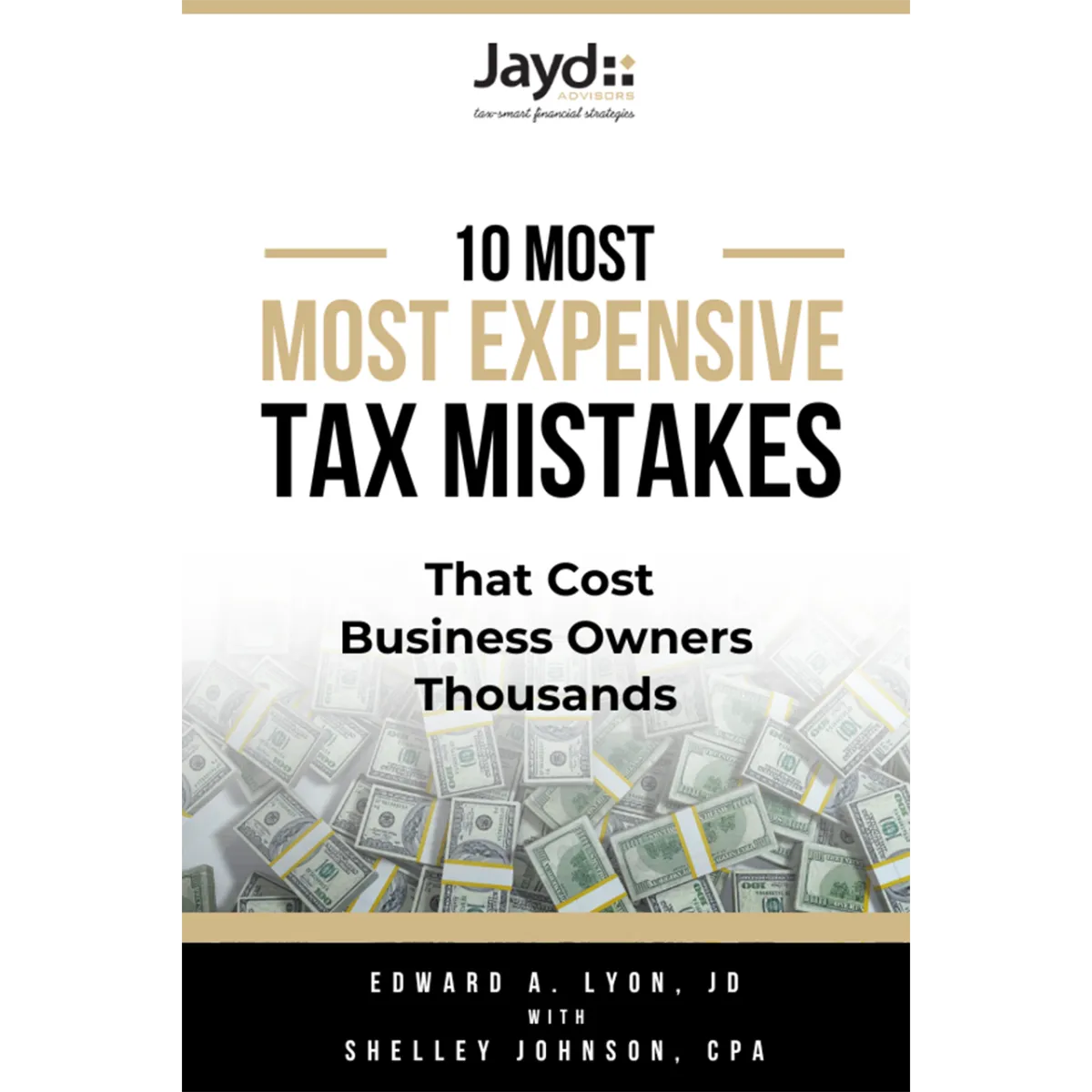

Stop Paying More Taxes Than Necessary

Avoid the 10 Most Expensive Tax Mistakes

Did you Know overpaying on taxes can accumulate into tens of thousands of dollars over time?

Don't let it happen to you! Act Now to Protect your Prosperity. Download a Free copy of our 10 Most E-Book Series.

Select Your Focus

To Begin Crafting Your Financial Future With Confidence

At Jayd Advisors, we are dedicated to helping you craft your financial future with confidence.

Contact Us

Carmel Office:

11350 North Meridian St.

Suite 120

Carmel, IN 46032

P: (317) 843-1040

F: 317-843-1090

Follow Jayd Advisors